Quick View: The Fed’s April Decision – More Than Meets the Eye

The following article was published by Janus Henderson, April 2026

Head of Global Short Duration and Liquidity Daniel Siluk explains why the Federal Reserve (Fed) has the latitude to be patient as it waits to see how the U.S.-Iran war impacts not only aggregate inflation but also growth prospects for the U.S. and the world.

Key takeaways:

- Keeping interest rates in their current range was largely a non-event at this week’s Fed meeting; the true story was seeking insight into how the central bank could react to a range of scenarios should energy prices remain elevated.

- With its relatively solid economy and energy independence, the U.S. finds itself in the enviable position of being able to exercise patience with respect to the war and its impact on prices and growth.

- Given the wide range of possible geopolitical – and thus economic – outcomes, we believe fixed income investors should use caution when considering adjusting duration and credit risk until the market gains greater clarity on how this crisis unfolds.

While reflections on how the duration and magnitude of higher energy prices may impact the Fed’s next policy action were at the center of this week’s meeting, an underlying – and perhaps understated – theme was the nature of the U.S. central bank’s monetary philosophy and approach to its dual mandate.

Evidence of this can be found in the lack of consensus among voting members in a continuing departure from Chairman Jerome Powell’s historical modus operandi of seeking to build consensus. On one side – as expected – was recent appointee Stephen Miran, who’s been anything but shy about his preference to cut rates. While not necessarily joining him, the majority of the Federal Open Market Committee voters did indicate a dovish bias. This seems to have become the central bank’s default in the absence of an obvious inflationary impulse – and as evidenced by 2022’s transitory call, sometimes not even then.

Three other dissenters did not want to go along with a dovish bias. We can categorize them as either adhering to the Fed’s historical data-dependent approach to setting policy or perhaps willing to send a salvo to presumptive incoming Chair Kevin Warsh, who has presented a case for secularly lower interest rates. And since Chairman Powell was understandably willing to go there, we will too by proposing that Fed members could be signaling that they view their independence from political influence as sacrosanct and that policy decisions are the result of a deliberative committee.

Giving energy prices the attention they deserve

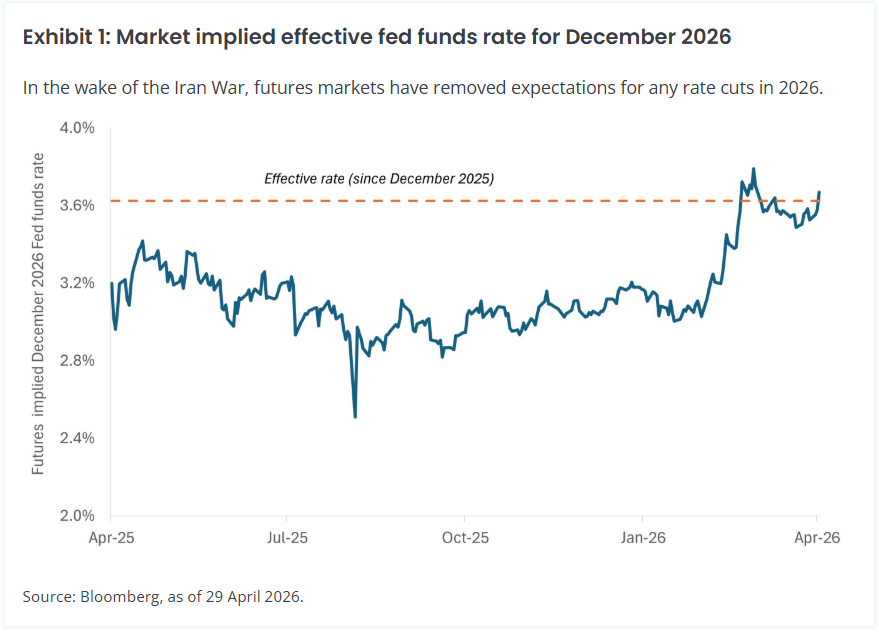

As the curtain possibly closes on the era of forward guidance, the Fed – as it had telegraphed – held its overnight benchmark rate steady, in a range of 3.50% to 3.75%. The continuation of pause deviated from the dovish script that had been laid out in late 2025. At that time, labor market softness intimated that the overnight rate could dip below 3.0% by the end of this year, as gauged by futures markets. In the wake of this week’s meeting, those same markets see no cuts for the remainder of the year.

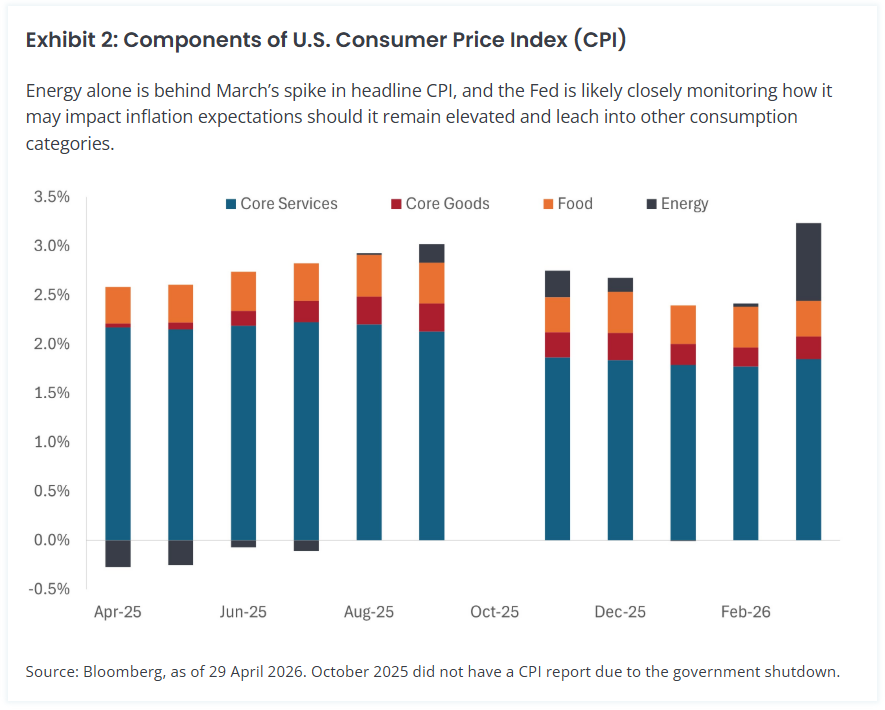

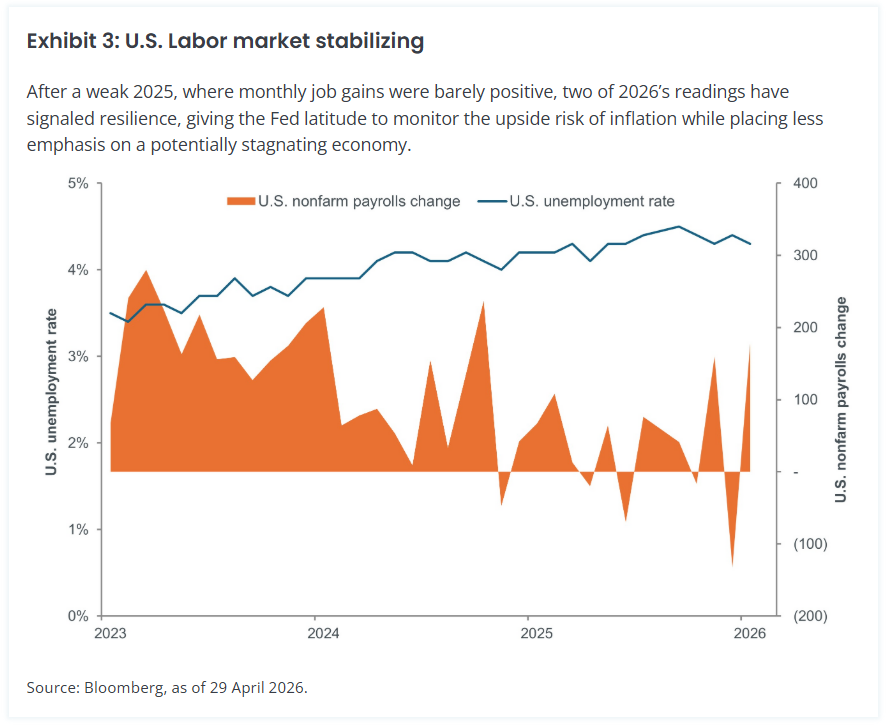

Two developments drove this change: The labor market has largely stabilized, and energy prices have surged in the wake of hostilities between the U.S. and Iran and the subsequent closure of the Strait of Hormuz. The market’s – and indeed the Fed’s – initial response was to look through higher oil prices, focusing instead on broader economic conditions.

The duration of the conflict and seemingly no easy resolution have broken those sanguine assumptions. Acutely aware of its botched transitory call four years ago, the Fed cannot dismiss the risk posed by higher energy prices leaching into core prices or, worse, impacting inflation expectations.

Fortunately for the Fed, solid economic expansion diminishes the tension that would have been otherwise felt in balancing the pillars of its dual mandate. Similarly, a stabilized labor market should lower the risk of a stagflationary environment that would force the Fed to make a difficult choice. We view current conditions as having bought time for the Fed as three possible scenarios play out:

- The conflict is resolved sooner than later, and energy prices revert to what had been a largely bearish environment of oversupply. This scenario would allow the Fed to look through a discrete inflationary surge.

- A prolonged period of energy prices seeps into broader inflation expectations, further pushing out what had been a bias to cut rates.

- Economic growth weakens as companies and households alter purchasing decisions in the wake of sustained higher prices. But even in this scenario, a rate cut is not guaranteed – likely owing to the Fed’s concern about allowing expectations to become unanchored.

Complicating matters for the Fed is that central banks are not in the business of managing supply-driven inflation. That said, the relative health of the U.S. economy and its energy independence should enable the Fed to be patient in seeing how these scenarios unfold, whereas other central banks may be forced to make tough decisions between containing prices and supporting growth. In fact, we believe the market has largely glossed over the risk to ex-U.S. growth posed by an extended military engagement and continued disruption of essential industrial and agricultural inputs.

But even in the U.S., tension between growth and inflation exists. And the longer this crisis plays out, the more that tension increases. Accordingly, we believe the bar has risen materially for any move: hike or cut.

Standing pat as the range of outcomes remains wide

Positioning portfolios to account for a geopolitical event with a wide range of possible outcomes is a challenge. As illustrated by shifting deadlines, a series of ultimatums, and the intransigence of the opposing sides, we believe investors, especially within fixed income, should be cautious about increasing risk – either duration or credit – at present. Certain jurisdictions may have no choice but to react to higher energy prices with rate hikes, especially if their central bank’s mandate prioritizes price stability. But as stated, the longer this crisis extends, the greater risk it presents to growth, especially in regions heavily dependent upon energy and other commodities imports.

Looking forward

With respect to U.S. monetary policy, we believe it’s too early to call a regime change at the Fed. Even if voting members shy away from forward guidance under a Chairman Warsh, we expect that voting members representing a range of views will continue to prioritize data dependence.

Implicit in that, however, should be the absence of a secular dovish or hawkish bias. In our view, holding fast to a 2.0% inflation target – which hasn’t been achievable in five years – may represent a dovish worldview that is hard to square with a $6.7 trillion balance sheet that would take significant time to wind down and in a period of deglobalization.

Importantly, investors must recognize that even subtle policy shifts would have meaningful ramifications for regional and global growth, inflation expectations, the yield curve, and the pricing of risk-free and risky assets.

About the Author

Daniel Siluk, Head of Global Short Duration & Liquidity | Portfolio Manager

Daniel Siluk is Head of Global Short Duration & Liquidity and a portfolio manager at Janus Henderson Investors, a role he has held since 2024. From 2009, Daniel was portfolio manager at Kapstream Capital, a subsidiary of Janus Henderson Investors, which acquired Kapstream in 2015. Prior to this, he served as manager of investment analytics at Challenger, a position he held from 2007 to 2009. While there, he provided attribution and risk metrics for the firm’s internal funds management business as well as their boutique partnerships, which included Kapstream. Before Challenger, he spent four years in London, where he implemented and tested attribution and risk systems for Insight Investment, the funds management arm of Halifax Bank of Scotland, and Northern Trust.

Daniel received a bachelor of applied finance degree from Macquarie University. He has 23 years of financial industry experience.

IMPORTANT INFORMATION

Energy industries can be significantly affected by fluctuations in energy prices and supply and demand of fuels, conservation, the success of exploration projects, and tax and other government regulations.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

This material has been prepared by Kapstream Capital Pty Limited (ABN 19 122 076 117 AFSL 308870) (Kapstream). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information.Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any rate of return nor capital invested are guaranteed.