The Opportunity in Securitisation Warehouses

Private securitisation warehouses, the pre-curser to public asset-backed securities, present a compelling opportunity for investors. Offering a substantial yield pickup over public markets due to their illiquidity and complexity, investors can gain attractive risk-adjusted returns and meaningful portfolio diversification benefits from this sub-asset class. Given its complex nature, it is critical to choose a manager with extensive experience in this market to ensure risks are managed appropriately.

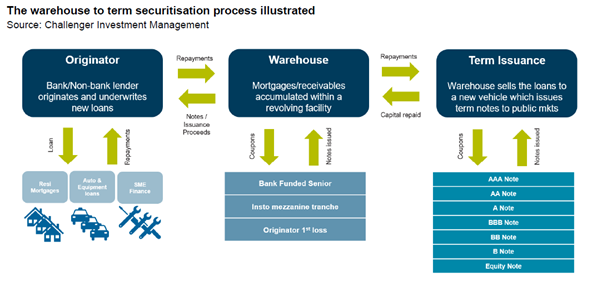

What are securitisation warehouses?

The term “asset-backed securities” refers to a pool of loans/receivables which are securitised and tranched into bonds of different risk/return profiles and issued in public markets. The underlying assets may be mortgages, auto loans, consumer loans or other types of debt. However, before the pool of assets can be securitised into public RMBS/ABS, the lender must accumulate a sufficient volume of loans to pool together. Warehousing, or pre-securitisation finance, allows a lender to accumulate a sufficient volume of loans before they are securitised and issued in public markets. As a result, they tend to be relatively short tenors, usually between 12-24 months.

The warehouse is tranched into the top senior tranche, the mezzanine tranche and the originator 1st loss/equity tranche. The senior financier of the top tranche is typically a bank who will also act as the arranger of the public transaction once sufficient loans have accumulated and the pool is ready to be securitised and publicly issued (step 3 in the diagram below). The lower equity tranche is usually funded by the originator of the loans.

Where has the warehouse lending opportunity come from?

Prior to the GFC, banks were willing to fund the senior and mezzanine tranches of a warehouse. However, in the period after the GFC, regulation and increased capital requirements have discouraged banks from funding anything other than the senior tranche. This left a structural gap in funding for the mezzanine tranche and alternative lenders like Challenger IM have stepped in to fund this space.

Why are warehouses such an attractive investment?

Warehouses provide an attractive pickup over public markets due to their illiquidity and complexity. Originators, or issuers of the loans, wish to get to public markets as quickly and efficiently as possible. To ensure this speed and efficiency, originators need to compensate the warehouse financiers. For alternative lenders like Challenger IM providing the mezzanine finance, the margins in warehouses are generally around 2% per annum higher than the margins in public term transactions of the same implied credit ratings.

How does Challenger IM approach warehouses?

While being an attractive investment, warehouses are highly complex structures where mezzanine tranches have capital at risk and 100 cents in the dollar can be lost in the case of default. Therefore, a manager needs to be highly experienced and skilled in this space to minimise risk of losses. Challenger has over a decade of experience investing in and structuring warehouse deals and is well versed in the appropriate intercreditor terms that are needed to reduce the risk to the lender if the underlying assets start to underperform.

Beyond investing as a lender, the team also has prior experience on the bank side structuring securitisation deals and the legal side working at law firms to document these warehouses. Challenger also has experience assessing an originator’s platform including their credit processes and regularly review their originators.

Furthermore, there are high barriers to entry for lenders, with scale and relationships key. Challenger has been in the market since 2010, building strong relationships with originators across Australia and New Zealand. Challenger also has the scale to grow the warehouse over time and even provide incremental capital to de-risk the senior tranche if required.

The Challenger IM Global ABS Fund provides clients access to private securitisation warehouses as part of a diversified portfolio of asset-backed securities. The Challenger IM Credit Income Fund and Challenger IM Multi-Sector Private Lending Fund also invest in private securitisation warehouses, with allocations of approximately 4% and 16% respectively as at February 2024.

The devil is in the detail

Separate from the general risk of default in the facility, there are several aspects of a warehouse that the lender must understand in detail. Challenger examines the precise terms of each warehouse deal to ensure it adequately protects the mezzanine lender, asking the below questions of each transaction.

-

Intercreditor terms: What can senior agree to without mezzanine consent? More aggressive documentation can cede all consent rights around document amendments, waivers and audits to the senior financier only, disadvantaging the mezzanine lender.

-

Enforcement rights: If the warehouse is not performing as expected, what are the rights of the senior financier? Can they enforce without mezzanine consent and if so, in what circumstances? What rights does the mezzanine financier have in an enforcement scenario?

-

Financial strength of the originator: If there is deterioration in the performance of the warehouse, what is the ability of the originator to rectify by adding subordination or buying back receivables?

-

Exit: How does the mezzanine lender exit the facility in the event that they need to without triggering an amortisation of the warehouse where senior is repaid in priority?

Given the complexity of private securitisation markets, it is important to take a detailed approach to assessing originators, underlying loan pools, as well as the structure and terms of a deal. Challenger IM has been investing in warehouses for over 10 years and is today a leading provider of private ABS solutions within Australia and New Zealand.

Challenger leverages its strong capabilities and experience in this space to offer investors access to its many benefits while seeking to minimise downside risks.

This document is prepared by Challenger Investment Partners Limited (ABN 29 092 382 842, AFSL 234678) (Challenger Investment Management or Challenger) the investment manager of the Challenger IM Global Asset Backed Securities Fund (Fund). The Fund is a sub-fund of the FundRock QIAIF Platform I ICAV.

In the United Kingdom this document is issued and approved by Fidante Partners Europe Limited (“Fidante Partners”). Fidante Partners is authorised and regulated by the Financial Conduct Authority in the conduct of investment business in the United Kingdom. In the European Union this document is issued and approved by Fidante Partners AB ("Fidante Sweden"). Fidante Sweden is an investment firm authorised by the Swedish Financial Supervisory Authority (Finansinspektionen). Fidante Sweden is authorised to provide investment advice, reception and transmission of orders and execution of orders on behalf of customers. Fidante Partners and Fidante Sweden are sub-distributors of the Fund and are issuing in this capacity only. Fidante Partners, Fidante Sweden and Challenger Investment Management are members of the Challenger Limited group of companies (Challenger Group). Information is intended to be general only and not financial product advice and has been prepared without taking into account your objectives, financial situation or needs. You should consider whether the information is suitable to your circumstances.

In Australia, this document is issued by Challenger and the minimum investment amount in Australia is A$500,000.

Unless otherwise stated, we do not guarantee any particular investment return, or the capital invested. We have taken reasonable care to ensure that any facts stated are accurate and any opinions given are on a reasonable basis, however you should take your own advice on the merits of these facts or opinions. In preparing this information, we have in part relied on publicly available information and third party sources believed to be reliable, however the information we provide has not necessarily been independently verified or audited. No part of this presentation may be reproduced or distributed in any manner without prior written permission of Challenger.

The information and opinions contained in this document are for background purposes only and do not purport to be full or complete. No reliance may be placed for any purpose on the information contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by Fidante or any of its affiliates or any vehicle and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is for information purposes only and does not constitute or form part of, and should not be construed as, an offer, invitation or inducement to purchase or subscribe for any units in the Fund nor shall it or any part of it form the basis of, or be relied upon in connection with, any contract or commitment whatsoever. It also does not constitute a recommendation regarding any investments. Recipients of this document who intend to apply for shares or interests in the Fund are reminded that any such application may be made solely on the basis of the information and opinions contained in the prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. The investments have not and will not be registered for sale, and there will be no public offering of the units. No offer to sell (or solicitation of an offer to buy) will be made in any jurisdiction in which such offer or solicitation would be unlawful.

Any forward-looking statements included in this presentation involve subjective judgment and analysis and are subject to significant uncertainties, risks and contingencies, many of which are outside the control of, and are unknown to, Challenger. In particular, they speak only as of the date of these materials, and they are subject to significant regulatory, business, competitive and economic uncertainties and risks. Actual future events may vary materially from forward looking statements and assumptions on which those statements are based. Given these uncertainties, recipients are cautioned not to place undue reliance on such forward-looking statements.

Historical returns are no guarantee of future returns and are not a reliable indicator of future performance. The money invested in the Fund can both increase and decrease in value and it is not certain that you get back all the invested capital. If you are in any doubt about the suitability of investing, you should seek independent advice. There are no entry or exit fees for the Fund.

UK investors only

This document is a financial promotion for the purposes of the Financial Services and Markets Act 2000 (FSMA) and has been issued for the sole purpose of providing information about the Fund. This document is issued in the United Kingdom only to and/or is directed only at persons who are of a kind to whom the Fund may lawfully be promoted by virtue of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (including authorised persons, high net worth companies, high net worth unincorporated associations or partnerships, the trustees of high value trusts and certified sophisticated investors). This document is exempt from the general restriction in Section 21 of FSMA on the communication of invitations or inducements to participate in investment activity on the grounds that it is being issued to and/or directed at only the types of person referred to above. Shares or interests in the Fund are only available to such persons and this document must not be relied or acted upon by any other persons.

European Union

In the European Union and the European Economic Area, this document is available to Professional Clients (as defined under Annex II to Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU).

Fidante and the Challenger entities are not authorised deposit-taking institutions (ADI) for the purpose of the Banking Act 1959 (Cth), and their obligations do not represent deposits or liabilities of an ADI in the Challenger Group (Challenger ADI) and no Challenger ADI provides a guarantee or otherwise provides assurance in respect of the obligations of Fidante and the Challenger entities. Investments in the Fund are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Accordingly, the performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any member of the Challenger Group.

Fidante Partners Europe Limited

Authorised and regulated by the Financial Conduct Authority Fidante

Registered Office: Bridge House, Level 3, 181 Queen Victoria Street, London, EC4V 4EG. Registered in England and Wales No. 4040660.

Fidante Partners AB

An investment firm authorised by the Finansinspektionen. Kungsgatan 8, SE-111 43 Stockholm, Sweden. Registered in Sweden No 559327-5497

The Fidante and Challenger entities are wholly owned subsidiaries of Challenger Limited, a company listed on the Australian Securities Exchange Limited.