Rising equity-bond correlation means it’s time to rethink portfolio construction

This article was originally published on Investor Daily on 9 June, 2026.

With the classic 60/40 portfolio now under pressure, liquid alternatives may offer investors a smarter way to diversify in uncertain markets.

Compound interest has famously been heralded as the ‘eighth wonder of the world’, but the same could equally be said of asset diversification. After all, the fact that an investor could allocate to a strategy with lower returns and higher risk, relative to their wider portfolio, and both increase their overall portfolio return and lower their total risk is in many ways wondrous.

The secret to this diversification benefit is a low return correlation, with this quality forming the basis for traditional multi-asset portfolios, most notably the ‘60/40’ portfolio, composed of 60% exposure to equities and 40% to bonds.

Correlation measures the degree to which asset prices move together. For much of the 20th century, a low positive correlation between equity and bond returns powered the success of the 60/40 approach, with bonds providing portfolios with income as well as partially diversifying equities in periods of market stress.

This relationship intensified from the late 1990s to the early 2020s, as the low-inflation, falling interest rate environment resulted in a negative correlation between equities and bonds. In this environment, demand-driven economic slowdowns were typically met with looser monetary policy, with falling rates supporting bond prices at a time when weaker growth expectations were weighing on equity markets. For many investors, this period reinforced the assumption that bond allocations would offset declines in equities.

In recent years, however, this dynamic has started to reverse. A shift to a higher-inflation, higher-interest rate, and more geopolitically uncertain world has seen the equity-bond correlation move back into positive territory. Unlike the demand-driven shocks of the previous era, recent crises have been shaped more by supply-side disruptions, where higher inflation weighs on both equities and bonds, and tighter monetary policy adds to the pressure – changes in interest rates, after all, do little to unblock the Suez Canal or demine the Strait of Hormuz.

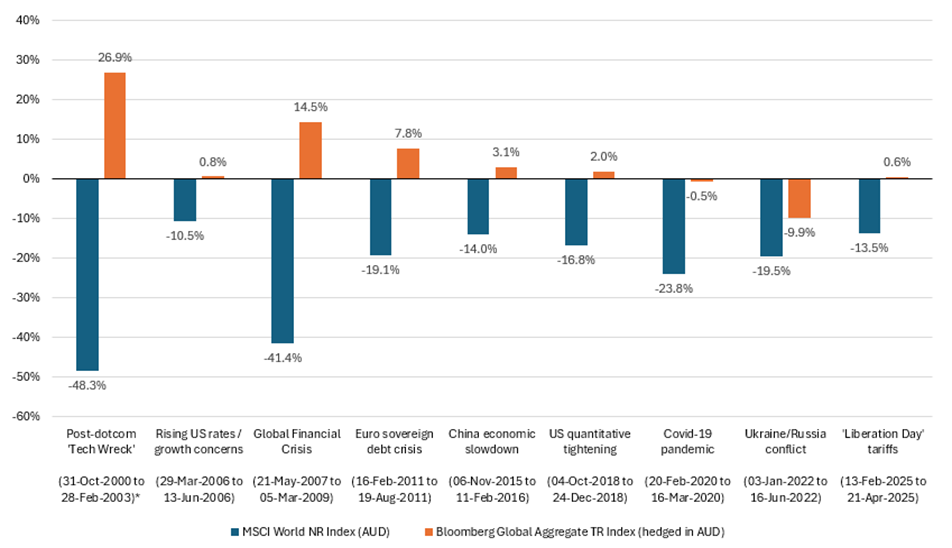

The chart below highlights this market dynamic, revealing that the degree to which bonds offset equity market drawdowns has diminished since the early 2000s. This culminated in 2022, when both asset classes fell simultaneously, resulting in a historically poor year for the 60/40 portfolio, and revealing the limitations of relying solely on equities and bonds for diversification.

Chart 1: Peak-to-trough performance of global equities and global fixed income in all equity market drawdowns greater than -10% since 2000

Source: Fidante, Morningstar Direct. ‘Global equities’ defined as the MSCI World NR Index in AUD. ‘Global fixed income’ defined as the Bloomberg Global Aggregate TR Index, hedged in AUD. *Monthly data used prior to 2004.

Building portfolios for the modern era

With the traditional 60/40 portfolio no longer providing the same level of diversification as in recent decades, investors are now seeking new sources of uncorrelated returns to mitigate risk and build more robust portfolios.

Liquid alternatives are particularly well placed to fill this gap. While no two strategies are exactly alike, liquid alternatives are united by their ability to access a wider set of return drivers than traditional investments. For example, non-directional strategies seek to generate returns based on the relationships between securities, irrespective of overall market direction, while alternative risk premia offer systematic sources of return that exist due to behavioural biases, market frictions, or risk transfer.

Owing to their differentiated return drivers, liquid alternatives tend to have low or negative correlations to traditional assets, offering valuable diversification. This attribute is particularly useful during periods of extreme market stress, where the ability to take both long and short positions, for example, increases the potential to provide downside protection.

A further advantage is flexibility. Unlike many private market strategies, liquid alternatives typically offer daily pricing and transparency, allowing investors to adjust allocations as conditions evolve. This is an increasingly valuable feature in a world where market environments can shift rapidly and unpredictably.

Focus on fundamentals

As with traditional asset classes, focusing on fundamentals is crucial when considering allocations to liquid alternative strategies. Outcomes can vary significantly depending on strategy design and risk management, meaning that selecting and partnering with high-quality managers with a clear investment edge remains critical.

When considering an investment in liquid alternatives, investors should also clearly define the funding source for allocations – that is, whether they will reduce their existing exposure to equities, bonds, or both to make room for a liquid alternative strategy in their portfolio. This decision can have significant impacts on overall return and risk outcomes and investors must select strategies accordingly.

Finally, risk tolerance is a crucial consideration. Liquid alternative strategies offer varying degrees of volatility, and it is important to have clarity on investment objectives and the strategy being employed. Investors should ensure the right liquid alternatives strategy is incorporated to deliver diversification in line with risk tolerance.

Solving a mounting challenge

As macro uncertainty persists, portfolio construction is becoming an increasingly challenging task for even the most experienced investors. Navigating markets in an uncertain world, building robust portfolios that can deliver returns more consistently over time, and mitigating risk have become lofty objectives in today’s investment environment.

Liquid alternative strategies can offer an intuitive way to unlock new sources of returns beyond equities and fixed income. While not a promise of outperformance, they are an important portfolio construction tool. Liquid alternatives expand the opportunity set by allowing investors to reallocate risk across a broader set of return drivers and complement traditional assets.

With the 60/40 portfolio coming under pressure, now may be the time for investors to give the traditional portfolio a modern-day rethink, and consider liquid alternative strategies that bolster diversification, unlock new sources of returns, and improve portfolio resilience.